Just read this on yahoo news. UK states they will write off cheques by 2018.

Granted, its fine if they want to write off cheques by 2018. But that's for their own country.

When I was in Australia, I barely even used the stack of HSBC cheques that I had... as it costs AUD1 to just even bank-in the cheque.Imagine if I wrote ten cheques, that'll be AUD10!

That's -- daylight robbery!. Not only do most of Aussie banks already charge a monthly fee, they charge "cheque processing fee".... >.<

Nonetheless, cheques are still well & alive in the Malaysia in day-to-day business. Malaysian businesses can't survive without the cheque-- as inter-bank transfers cost a bomb (RM2 per transaction) each, whereas it's free in Australia.

Hmmm..

Wednesday, December 16, 2009

Tuesday, December 8, 2009

The case of the Merchant Foul.

I had the experience of a participating merchant, whom we shall name as Merchant Foul, this round who tried to "play foul" in the exhibition.

The History: In the previous exhibition that this merchant joined us with, they were given a "free" booth, or in other words, "space" to place their ware which they need not had to pay a premium for.

A month before the next exhibition due, a staff from their team called my office enquiring if the booth next to theirs was still vacant. I informed them that it was still vacant. But she did not press me for further details thereafter.

The Scenario: The day of the exhibition came. Lo and behold, I get a call from the same merchant with the query that "why had the booth next to theirs cordoned off when I had told them it was vacant" a month ago?

I was surprised she had the gall to even ask me that.

Then it came to the Organiser's attention that this particular merchant had designed a booth which occupied the area equivalent for three booths!

Rationale:

Let me ask you, would you create the design for a booth for the size of three booths when you had only paid the rent for two? Then you as the customer came in hoping that the Organiser would give the extra booth (beside yours) to you for free?

Indeed, it is the perogative of the Organiser to not charge a merchant- that is in the event that there are no takers. In fact, this particular merchant had one "flaw" in their argument. If they had known that the booth next to theirs was vacant, they should have informed the Organiser that they wanted it.

Their Bullets:

On the same evening of the setup days, a few representatives from their side came to the Organiser's booth and tried to bamboozle us to give up the booth beside theirs to them. They even tried to maneuver the Organiser into allowing them to move their ware into the thoroughfare, but that would mean a compromise of the public safety which would not be tolerated. !

We promptly told them off.

The next morning, their Lady Manager came to us again. We told them off. The Lady Manager walked off in a huff with her tail between her legs.

Conclusion: The merchant next to theirs refused to budge. Merchant Foul had to pay for the rent of the booth on the other side of the same area.

I hope they learn their lesson well. !

The History: In the previous exhibition that this merchant joined us with, they were given a "free" booth, or in other words, "space" to place their ware which they need not had to pay a premium for.

A month before the next exhibition due, a staff from their team called my office enquiring if the booth next to theirs was still vacant. I informed them that it was still vacant. But she did not press me for further details thereafter.

The Scenario: The day of the exhibition came. Lo and behold, I get a call from the same merchant with the query that "why had the booth next to theirs cordoned off when I had told them it was vacant" a month ago?

I was surprised she had the gall to even ask me that.

Then it came to the Organiser's attention that this particular merchant had designed a booth which occupied the area equivalent for three booths!

Rationale:

Let me ask you, would you create the design for a booth for the size of three booths when you had only paid the rent for two? Then you as the customer came in hoping that the Organiser would give the extra booth (beside yours) to you for free?

Indeed, it is the perogative of the Organiser to not charge a merchant- that is in the event that there are no takers. In fact, this particular merchant had one "flaw" in their argument. If they had known that the booth next to theirs was vacant, they should have informed the Organiser that they wanted it.

Their Bullets:

On the same evening of the setup days, a few representatives from their side came to the Organiser's booth and tried to bamboozle us to give up the booth beside theirs to them. They even tried to maneuver the Organiser into allowing them to move their ware into the thoroughfare, but that would mean a compromise of the public safety which would not be tolerated. !

We promptly told them off.

The next morning, their Lady Manager came to us again. We told them off. The Lady Manager walked off in a huff with her tail between her legs.

Conclusion: The merchant next to theirs refused to budge. Merchant Foul had to pay for the rent of the booth on the other side of the same area.

I hope they learn their lesson well. !

The Occupational Health & Safety Concerns of Exhibitions

In any venue that has public access, many details need to be looked at as it concerns the safety of the public.

1) Security of the Venue where exhibition will take place:

- Gates to be locked at night to adjoining exits and entrances. They can only be opened during joint openings.

- Valuable items are to be kept away.

- Participating exhibitors at no time are allowed to have access to the venue's security CCTV recording, unless permission is granted by the venue's security in the event that security has been compromised.

- Participating merchants should immediately inform the Organiser, who in turn will immediately inform the Venue owner in case of suspect of any incidents.

2) Common area cleaning:

- Cleaning Fees are chargeable for all Hall areas throughout the days of the exhibitions based on number of staff required.

3) Cargo lift operator and furniture setting up:

- Individuals required for per setting up type.

Number of Co-ordination meetings required prior to due Exhibition time:

4) Licensing & Permission from the relevant Authorities

- DBKL Floor licence, DBKL- (License granted by the City Hall that states the exhibition is 'legal')

- Floor plan of venue shows primary, exit and emergency exits. In other words, floor plan of venue must adhere to fire escape routes as safe in the event of an emergency.

- Show welcome arch, AV Console equipment

- Going through every booth for the possibility of merchants placing gas tanks (that could compromise public safety)

- That all Lamp Post buntings needs DBKL (City Hall) licensing authority code.

- The number of A&P 'equipment" as allowed by the venue's management around the venue's location.

5) Handover & Take Back of Venue:

- Is a joint inspection between 3 parties- the management of the Venue, the Organiser, and the Contractor.

- Check lists & records of initial venue condition

- Photos taken as record of venue condition.

Other areas include:

- Floor Loading, Floor protection, Carpeted area guidelines.

- Passes for individual participating staff entry.

1) Security of the Venue where exhibition will take place:

- Gates to be locked at night to adjoining exits and entrances. They can only be opened during joint openings.

- Valuable items are to be kept away.

- Participating exhibitors at no time are allowed to have access to the venue's security CCTV recording, unless permission is granted by the venue's security in the event that security has been compromised.

- Participating merchants should immediately inform the Organiser, who in turn will immediately inform the Venue owner in case of suspect of any incidents.

2) Common area cleaning:

- Cleaning Fees are chargeable for all Hall areas throughout the days of the exhibitions based on number of staff required.

3) Cargo lift operator and furniture setting up:

- Individuals required for per setting up type.

Number of Co-ordination meetings required prior to due Exhibition time:

4) Licensing & Permission from the relevant Authorities

- DBKL Floor licence, DBKL- (License granted by the City Hall that states the exhibition is 'legal')

- Floor plan of venue shows primary, exit and emergency exits. In other words, floor plan of venue must adhere to fire escape routes as safe in the event of an emergency.

- Show welcome arch, AV Console equipment

- Going through every booth for the possibility of merchants placing gas tanks (that could compromise public safety)

- That all Lamp Post buntings needs DBKL (City Hall) licensing authority code.

- The number of A&P 'equipment" as allowed by the venue's management around the venue's location.

5) Handover & Take Back of Venue:

- Is a joint inspection between 3 parties- the management of the Venue, the Organiser, and the Contractor.

- Check lists & records of initial venue condition

- Photos taken as record of venue condition.

Other areas include:

- Floor Loading, Floor protection, Carpeted area guidelines.

- Passes for individual participating staff entry.

The Technical How-To of Managing An Exhibition

The last weekend has been a hectic one for me. The company that I work for had their second partnership with an international bank. Here are some details that one will need to know to ensure that an exhibition runs well.

Pre-Exhibition Measures for the day:

- Provide a limited refreshments to the exhibitor- as an 'emotional assurance' that the organiser is looking after the participants.

- Security and Organiser has early-day-walk to ensure that safety of merchants ware have not been compromised.

- Security and Organiser have walk to ensure that all walkways are clear and safe for the public to access to. All cables and wires are neatly in place in main thorooughfare to avoid the public from falling over or injury themselves.

- To ensure that only participating merchants, and organiser has access to the exhibition venue before the show. Individuals without the proper authority to come in (i.e. exhibition name tags) is not to be allowed in at any time as this will compromise the safety of all parties involved.

During The Exhibition:

Three aspects of the technical aspect had to be looked at to ensure that the telecommunications and network lines run smoothly.

1) Payment terminals run smoothly- Merchants need to have staff who are able to operate credit card terminals. This includes pre-exhibition training to ensure time is not wasted during the sale process.

2) Electricity supply does not short circuit- An electricity trip is the result of overload usage, especially by merchants that decide to run electrical appliances.

It is also the worst thing to happen in the midst of a credit card transaction, as it could result in the loss of "sale" as well.

3) Phone lines are working- In the event that the bank is unable to provide a "wireless" terminal, phone lines are necessary. Further, wireless credit card terminals are limited in the application & functionality.

Phone lines which are "offline" will cause the credit card terminals to not work. Hence it could occur in the loss of a "sale".

From here, it could be seen that three aspects- telecommunication cables and electricity supply, as well as trained staff is required to operate the credit card terminals.

4) Technical Support- Another overlooked aspect is that the bank should provide adequate staff in the case of technical support for the usage of the credit card terminals.

Usage of credit card terminals includes functions of

- checking reward points amount,

- knowledge of keying card to redeem points for purchases,

- doing the daily transaction summary for the day.

5) Network support for technical failures-

- the speed of support in the event of electricity trip

- the speed of support in the event of credit card in-accessability.

6) Methods of illiciting sales & transactions by participating merchants

- to ensure that all merchants play fair, by ensuring that they do not utilize audiovisual equipment that will cause economic damage to another merchant, or cause another merchant to complain.

- to ensure that all merchants have 'open line of access' to the organiser in the event of a 'foul play" by other participating merchants.

- to ensure that security and organiser take strict action against merchants who violate rules & regulations.

- in the midst of the crowd & sales, there will be "illegal" merchants- who will try to come in and sell their ware "unannounced", and without going through the proper channels. This will not only compromise the safety of the public, but also the economic output of the "legal" merchants in the exhibition concerned. In this situation, the venue security will be summoned to remove these individuals.

7) Safety of public is not to be compromised.

- All buntings or ware displayed does not compromise the safety of the public, i.e helium balloons, & thoroughfare is to be always clear.

End of the Day Measures:

- Security & staff to take the end-of-the-day walk to ensure that all things are kept.

- 'Loose ends to be tied'- hanging cables (if ever any), and other details.

Pre-Exhibition Measures for the day:

- Provide a limited refreshments to the exhibitor- as an 'emotional assurance' that the organiser is looking after the participants.

- Security and Organiser has early-day-walk to ensure that safety of merchants ware have not been compromised.

- Security and Organiser have walk to ensure that all walkways are clear and safe for the public to access to. All cables and wires are neatly in place in main thorooughfare to avoid the public from falling over or injury themselves.

- To ensure that only participating merchants, and organiser has access to the exhibition venue before the show. Individuals without the proper authority to come in (i.e. exhibition name tags) is not to be allowed in at any time as this will compromise the safety of all parties involved.

During The Exhibition:

Three aspects of the technical aspect had to be looked at to ensure that the telecommunications and network lines run smoothly.

1) Payment terminals run smoothly- Merchants need to have staff who are able to operate credit card terminals. This includes pre-exhibition training to ensure time is not wasted during the sale process.

2) Electricity supply does not short circuit- An electricity trip is the result of overload usage, especially by merchants that decide to run electrical appliances.

It is also the worst thing to happen in the midst of a credit card transaction, as it could result in the loss of "sale" as well.

3) Phone lines are working- In the event that the bank is unable to provide a "wireless" terminal, phone lines are necessary. Further, wireless credit card terminals are limited in the application & functionality.

Phone lines which are "offline" will cause the credit card terminals to not work. Hence it could occur in the loss of a "sale".

From here, it could be seen that three aspects- telecommunication cables and electricity supply, as well as trained staff is required to operate the credit card terminals.

4) Technical Support- Another overlooked aspect is that the bank should provide adequate staff in the case of technical support for the usage of the credit card terminals.

Usage of credit card terminals includes functions of

- checking reward points amount,

- knowledge of keying card to redeem points for purchases,

- doing the daily transaction summary for the day.

5) Network support for technical failures-

- the speed of support in the event of electricity trip

- the speed of support in the event of credit card in-accessability.

6) Methods of illiciting sales & transactions by participating merchants

- to ensure that all merchants play fair, by ensuring that they do not utilize audiovisual equipment that will cause economic damage to another merchant, or cause another merchant to complain.

- to ensure that all merchants have 'open line of access' to the organiser in the event of a 'foul play" by other participating merchants.

- to ensure that security and organiser take strict action against merchants who violate rules & regulations.

- in the midst of the crowd & sales, there will be "illegal" merchants- who will try to come in and sell their ware "unannounced", and without going through the proper channels. This will not only compromise the safety of the public, but also the economic output of the "legal" merchants in the exhibition concerned. In this situation, the venue security will be summoned to remove these individuals.

7) Safety of public is not to be compromised.

- All buntings or ware displayed does not compromise the safety of the public, i.e helium balloons, & thoroughfare is to be always clear.

End of the Day Measures:

- Security & staff to take the end-of-the-day walk to ensure that all things are kept.

- 'Loose ends to be tied'- hanging cables (if ever any), and other details.

Thursday, December 3, 2009

The Pavillion: Mastercard Malaysia Airlines GWP Promotion.

As per this entry, this is the information as provided from Pavilion for their current Mastercard-Malaysia Airlines Promotion.

*All Items Are Available Whilst Stocks Last!

1st tier: For RM500 purchases.

L’Occitane – Aromachologie range

5 items in box:

- Milk Extra Gentle Soap – 50grms

- Body Lotion - 35ml

- Shower Gel - 35ml

- Conditioner - 35ml

- Shampoo - 35ml

- Amino Acid Shampoo – 65ml

- Deluxe Hand & Body Lotion - 65ml

Crabtree & Evelyn

5 variety to choose from

- Summer hill

- Lavender

- Gardeners

- La Source

- Rose Water

For more detailed & updated news on the above promotion, please call Pavillion KL: General Line/ Concierge Services enquiries: +603- 2118 8833.

It was not my intention to write this entry. However, for the service of my beloved

Having to choose between the blogs, I decided this entry best fit here as continuity of the Debit Mastercard saga. ^^

Tuesday, December 1, 2009

Follow Up: Royale Christmas@ Pavillion KL Mastercard Debit Incident.

Pavillion Brochure- inside of card brochure 1

Inside of Card Brochure 2

This is an update of this entry that I made of my incident recently at the Pavillon KL.

This afternoon, at about 13:30 hours, I made hardcopies of all related electronic publications & communications that I had initiated & published. Then via fax, I forwarded the copies to the Marketing Department of Pavillon KL.

Around 17:45 hours, I received a call from their Concierge Manager. He proceeded to inform me

I will update this post as when more news is received.

This afternoon, at about 13:30 hours, I made hardcopies of all related electronic publications & communications that I had initiated & published. Then via fax, I forwarded the copies to the Marketing Department of Pavillon KL.

Around 17:45 hours, I received a call from their Concierge Manager. He proceeded to inform me

- that he had contacted Mastercard.

- he was informed that the usage of the Mastercard Debit is valid under the Mastercard Worldwide umbrella.

He didn't mention the other Mastercard types though. (so, what does that mean then?)- He later said that is encompasses all Mastercard range. I sure hope so!

- He reserved the 'instant free gift' for me.

- For the Mastercard- Malaysia Airlines Promotion: Three options to choose the 'instant free gift'- for Tier 1 from: (purchases of RM500) - Loccitane gift set, Kiehl's gift set, or 2 mugs for Mastercard users. I chose the Kiehl's set. (I know this is good news for all the beauty skincare users who frequent these blogs!)

- The Tier 2 promotion is for purchases RM1000 and above.

No idea what the instant gifts are though.I was told that the Tier 2 instant gifts had 4 range of products from Crabtree & Evelyn....

- I was also told at the counter that receipts & spending for the Mastercard promotion above is accumulative, but must be on the same card within the same day. Which means, two persons can accumulate their spending, and share the instant free gift. The redemption is limited to one per customer per day.

- If I remember rightly too, the promotion is not extended to purchases from Parkson Pavillion,

& possibly Tangs, but ONLY individual outlets, and includes both retail & dining establishments. This is possibly due to the RM10 voucher giveaway with RM100 purchase at Parkson Pavillion.

I will update this post as when more news is received.

Saturday, November 28, 2009

Royale Christmas @ Pavillion KL: Mastercard Debit Not Accepted.

I feel marginalized. and upset.

Let me tell you what happened today.

It is stated on the first brochure (Pavillion Brochure 1) "Get an instant free gift with RM500 charged to any Mastercard Worldwide". As far as the general public is concerned, we are led to believe that Mastercard Worldwide consists of ALL Credit-cards, Debit, Prepaid and Electronic cards under the Mastercard brand.

Here are some questions that I realised:

From here, it can be seen that the Management from Mastercard is clearly misrepresenting their brand.If Mastercard's Management has no intention of rewarding other card type users, they should have stated clearly in the brochure, and added a disclaimer, as this brochure is given to the general public.

I demand an answer from Mastercard. and Pavillion. It is not a small amount that I have spent, and as a customer, I would have thought that the Mastercard in Malaysia would be honest in its advertising.

Why has the Management from Pavillion allowed the brand Mastercard to provide such misleading information in their brochure, and not treat their customers right?

This misrepresentation causes me to think that the Management of Mastercard has the intention of misleading other Mastercard card type users with no intention of honouring their promotion. Don't you agree so?

If this is the way the misleading advertising has been done, both parties (Mastercard & Pavilion) had better provide some good explanation for us.

This has been a really unsavory experience, and definitely does not feel like a very "Royale Christmas @ Pavillion KL" at all!

Follow Up Entry: The Concierge Manager Called.

Let me tell you what happened today.

Can you see the part "Card Type: Mastercard" there?

The promotion that goes in Pavillion printed in their Royale Christmas@Pavillion KL is as follows:

"Get an instant free gift with RM500 charged to any Mastercard Worldwide" .

The Instant Free Gift? A Loccitane or Kiehl's Gift Set, which in retail price, is worth more than RM130, given to any "Mastercard Worldwide" holders with the purchase of RM500.

Today I had made a payment in full, amounting to more than RM500 (RM770) purchase at one of the swanky ladies salon at Seventh Heaven in Pavillion. Yet, I was informed that because it was a Mastercard Debit, I was not entitled to the instant free gift.

"Get an instant free gift with RM500 charged to any Mastercard Worldwide" .

The Instant Free Gift? A Loccitane or Kiehl's Gift Set, which in retail price, is worth more than RM130, given to any "Mastercard Worldwide" holders with the purchase of RM500.

Today I had made a payment in full, amounting to more than RM500 (RM770) purchase at one of the swanky ladies salon at Seventh Heaven in Pavillion. Yet, I was informed that because it was a Mastercard Debit, I was not entitled to the instant free gift.

Pavillion Brochure-inside of card brochure 1

Pavillion Card- inside of brochure 2

Pavillion outside brochure 3

It is stated on the first brochure (Pavillion Brochure 1) "Get an instant free gift with RM500 charged to any Mastercard Worldwide". As far as the general public is concerned, we are led to believe that Mastercard Worldwide consists of ALL Credit-cards, Debit, Prepaid and Electronic cards under the Mastercard brand.

Here are some questions that I realised:

- The brochure DID NOT state which card, country, card type but just "any Mastercard Worldwide".

- So, does that mean Mastercard Debit does not fall under the "Mastercard Worldwide" umbrella?

- Does that also mean Mastercard Debit users are not Mastercard users?

From here, it can be seen that the Management from Mastercard is clearly misrepresenting their brand.If Mastercard's Management has no intention of rewarding other card type users, they should have stated clearly in the brochure, and added a disclaimer, as this brochure is given to the general public.

I demand an answer from Mastercard. and Pavillion. It is not a small amount that I have spent, and as a customer, I would have thought that the Mastercard in Malaysia would be honest in its advertising.

Why has the Management from Pavillion allowed the brand Mastercard to provide such misleading information in their brochure, and not treat their customers right?

This misrepresentation causes me to think that the Management of Mastercard has the intention of misleading other Mastercard card type users with no intention of honouring their promotion. Don't you agree so?

If this is the way the misleading advertising has been done, both parties (Mastercard & Pavilion) had better provide some good explanation for us.

This has been a really unsavory experience, and definitely does not feel like a very "Royale Christmas @ Pavillion KL" at all!

Follow Up Entry: The Concierge Manager Called.

Monday, November 9, 2009

Debit Mastercard: Better Than Cash?

(Don't you think these cards just look enticing to make you go out and shop further?)

It was not too long ago in Malaysia that Visa had a huge marketing campaign promoting the usage of Visa Debit cards...

But with Visa in the money-making game, it is a given that Mastercard will not want to lose out in getting a part of the lucrative pie which is "money". Even Debit Mastercard would not be able to escape the money driven race.

Granted, I am quite happy to know that Maybank has a version of the Debit Mastercard.

Though, I have yet to convert my yellow ATM e-debit Maybankard to either Visa, or Mastercard Debit. That makes almost all my cards coming completely from one bank, except for the one Citibank Debit Visa that I have.

I would agree with the "no more ATM queues and no more hassle with everyday purchases, no more losing track of your expenditure. ".

However, I really disagree with the tagline "Better Than Cash". They should not be allowed to trademark it.

When one does not possess a Credit Card, other people (who are in the money-making business) would not be able to tempt us to buy items based on a credit facility.

I have been to beauty salons carrying just cash, and a single debit card, knowing that no matter what does sales people do or say, they can't make me buy anything I do not want.

Indeed the credit card is a "credit facility" used when we are tempted to pay for an item we desire based on the "buy now, pay later" philosophy. Spending our future money.

How could Debit Mastercard be better than cash?

Merchants utilize the EPP (Easy Payment Plan) to make paying for a product or services look attractive. Perhaps "that" is the "enticing bait". Preferably, though so, I must admit that the credit card is a useful credit facility, as it provides 30 up to 55 days interest free loan, and when we pay before it is due.

I would use a credit card to buy goods with high-risk factor. (i.e a company retailing a product that may go bankrupt, buying from online malls, E-Bay, and airline tickets).

Utilized wisely, I would be able to buy that nice facial treatment package from Sothys or Clarins amounting to RM600 in two instalments. Hopefully by the time the second instalment comes around, I'd have enough money to pay for it...

But cash is good when I am thinking of getting goods with a Heavy Cash Discount. Yes, everything is negotiable when the price is high, and the payment method used is Hard Cold Cash.

I really love it.

Entry dated: 7th Nov 09

Sunday, November 8, 2009

Citibank: Hilton PJ Paya Serai Buffet Dinner Promotion.

Paya Serai Hilton PJ

Today I was at Hilton PJ for a Buffet Dinner with staff from my mother's work place. It seems that this restaurant, Paya Serai has a special promotion for all its Citibank card holders.

The terms & conditions of the promotion:

- Price per paying patron is RM81+ (including 5% GST and 10% service charge).

- Promotion per paying patron is 1 + 1 (Buy One, Get One Free)

- Promotion valid till 26th April 2010

- Promotion valid only for Buffet Dinner (Sunday & Monday nights only)

- Promotion valid to all Citibank cardmembers (Credit Card & Visa Debit)

Yes, this is a special for all Citibank cardmembers, including Citibank Visa Debit cardmembers. I really appreciate the fact that Citibank is taking it all out to include the non-credit cardmembers in the promotion as well.

How Was The Food?

The food was fairly serviceable. I can't say much about the food as I already had eaten earlier at Secret Recipe (chicken stew, chocolate cheesecake, flat white coffee, and garden salad) with one of my clients earlier, and could not stomach much of the buffet..

The galore of food available was from local cuisine (chinese, indian, malay), international cuisine like western garden salads, cream soups, cheese & crackers, pasta, and the normal dessert fare of kueh & fruits. I had an order of watermelon juice (which seemed to be freshly squeezed from what I could see), but did not check to see if it was included in the buffet range available.

Nonetheless, the attendees who went seemed fairly happy with the galore of food provided. For a 1+1 promotion, its is fairly satisfactory value for money, and seems brighter & cleaner than the so-called upclass Japanese buffet by Jogoya Starhill.

Location: Hilton Petaling Jaya,

No 2 Jalan Barat, Petaling Jaya, Malaysia 46200

Tel: 60-3-7955-9122

Fax: 60-3-7955-3909

Thursday, November 5, 2009

Australia: Introducing Wizard Clear Advantage Mastercard

When my friend Elena was in Kuala Lumpur early this year, we had gone shopping to Mid Valley Megamall. She mostly shopped for items which were not as easily accessible to in Australia.

Elena had brought along this card, called the Wizard Clear Advantage Mastercard. She described the card as useful as the card did not charge for overseas foreign transactions (foreign here meaning Malaysia), and conversion was done instantaneously. This was useful on the days when the Australian Dollar was high compared to foreign currencies.

This card is a credit facility provided by GE Finance Australia. Among some of the features of this card are:

- ZERO Annual Fee

- 4.99 % P.A for six months on balance transfer from the date of opening.

- Cash Advance Facility available.

- The standard 55 interest fee free days on purchases.

- Annual Interest Rate 18.49 %

I seriously think this card is extremely economical and useful. When I was travelling to South Korea and Japan, I had brought along my HSBC Visa Debit and CommSec Mastercard Debit. The HSBC Visa Debit charges a hefty fee for foreign transactions, where-as the CommSec Mastercard Debit charges a sizable conversion rate..

You could guess that I did not really use much of both cards, except for that one time during an emergency when I was already leaving for Japan and had lost of my korean won. I had no alternative but to use the HSBC Visa Debit-- when I looked at the statement a month later, I realised that I was charged about AUD4+ for that one transaction. A hefty fee indeed!

So yeah, to travellers, I'd recommend this card, if only to save on foreign transaction fees, and conversion charges as well. ^^

For more information about this card, click here.

Saturday, October 24, 2009

Sales Strategy: Waiting the Customer Out.

I have had a number of clients who have been really pushy, and demanding. I am in what is described as the 'rent-space-for-showcase' business. These clients have demanded high discounts, and good allocations from us on the supplier side. Some had even informed me that they were willing to let go of taking part in the showcasing project initially.

As their demands had been what is deemed excessive, I decided to take a step back. Indeed, one would call my way as 'not being pushy'. So much so, I had taken my own sweet time to get back to them. Yet, the places allocated to these guys is pretty much prime spots.

Perhaps, for some, this approach would not work, as there will be other clients who are serious about participation. I discerned that this guys were going for the 'waiting game'. The party that relents

the first will lose. Finally, they called up, and asked how they were supposed to join.

The ball was definitely in my favour. Yes, as you can see, pushy does not work each time.

As their demands had been what is deemed excessive, I decided to take a step back. Indeed, one would call my way as 'not being pushy'. So much so, I had taken my own sweet time to get back to them. Yet, the places allocated to these guys is pretty much prime spots.

Perhaps, for some, this approach would not work, as there will be other clients who are serious about participation. I discerned that this guys were going for the 'waiting game'. The party that relents

the first will lose. Finally, they called up, and asked how they were supposed to join.

The ball was definitely in my favour. Yes, as you can see, pushy does not work each time.

Thursday, October 22, 2009

Malaysia: Introducing Maybank Mastercard Platinum Debit

The joke of the day lies in the fact that Maybank Visa Debit already has a cherry background, and here is Maybank trying to introduce a "Platinum" status card to the Mastercard Debit, where customers have already associated the cherry with the Visa Debit.... man, you guys need to get creative.

All black is better than all cherry.

Click here for more information.

Malaysia: Bankcard/E-Debit System Not Very STABLE!

From my previous experience of using my Maybank Bankcard or e-debit card (as they call it in Malaysia) I have found that a lot of terminals have problem with the system.

THE SCENARIO

I had made a transaction on an EON bank card terminal. The amount swiped was Rm1,000.00. However, the terminal did not print out the receipt, as per the normal. Yet, when I checked on my online banking, I found out that Rm1,000.00 had already been transferred over to card terminal account..

Fortunately, the merchant was kind enough to "reserve" the transaction for me. For the next two weeks thereafter, I was living from hand-to-mouth.. as my bank account had almost zero savings... and had to call the bank up to expedite the refund of my monies.

From discussions with friends who have used the Bankcard/E-Debit feature, it seems that it is an occuring problem amongst the other E-Debit cards as well....

CONCLUSION

In return, I have found that the cards with the VISA or MASTERCARD logos are much more reliable, with less terminal error problems occuring. Although they are not as safe as the E-Debit cards, well...

I now keep the E-Debit cards for the purpose of money withdrawal, and the occasional small amount purchases..

THE SCENARIO

I had made a transaction on an EON bank card terminal. The amount swiped was Rm1,000.00. However, the terminal did not print out the receipt, as per the normal. Yet, when I checked on my online banking, I found out that Rm1,000.00 had already been transferred over to card terminal account..

Fortunately, the merchant was kind enough to "reserve" the transaction for me. For the next two weeks thereafter, I was living from hand-to-mouth.. as my bank account had almost zero savings... and had to call the bank up to expedite the refund of my monies.

From discussions with friends who have used the Bankcard/E-Debit feature, it seems that it is an occuring problem amongst the other E-Debit cards as well....

CONCLUSION

In return, I have found that the cards with the VISA or MASTERCARD logos are much more reliable, with less terminal error problems occuring. Although they are not as safe as the E-Debit cards, well...

I now keep the E-Debit cards for the purpose of money withdrawal, and the occasional small amount purchases..

Singapore: Citibank ATMs abound only in shopping malls.

I thought my eyes were about to pop.. at almost every major shopping establishment in Singapore that I went to, I could practically find a Citibank ATM.

As most may know, I currently hold a Citibank Visa Debit card. I applied for this card after being told that the conversion rates for this card is low, and fee-free as well.

As of date, I have yet to find many Citibank ATMs around any of the shopping malls around Kuala Lumpur, and could never withdraw any money since it is considered a foreign card (RM10 chargeable for withdrawals! How crazy is that!).

The only time I have ever used my Citibank Visa Debit around KL is when I had needed to make payments at the counter....

Perhaps Singapore is less strict on foreign banks, but in Malaysia, it is hard to find many Citibank branches around here.. and the nearest one is in Puchong, where I had made a complaint about their service! So the only way I could transfer money to my Citibank savings account was through bank-to-bank transfer, and that costs RM2 per transaction (free in Australia).

It was a pity that I could not find a single Citibank ATM at the Changi International Airport, although there was a humongous annoying big Citibank bunting right in the middle of their departures terminal.

How deceiving that was! I ended up exchanging my Australian dollars (since Australian and Singapore currently have almost similar exchange rate) at the exchange bureau in the airport and at Chinatown (better cash rates), and not using my Citibank Visa Debit card thereafter.

Oh Well.

As most may know, I currently hold a Citibank Visa Debit card. I applied for this card after being told that the conversion rates for this card is low, and fee-free as well.

As of date, I have yet to find many Citibank ATMs around any of the shopping malls around Kuala Lumpur, and could never withdraw any money since it is considered a foreign card (RM10 chargeable for withdrawals! How crazy is that!).

The only time I have ever used my Citibank Visa Debit around KL is when I had needed to make payments at the counter....

Perhaps Singapore is less strict on foreign banks, but in Malaysia, it is hard to find many Citibank branches around here.. and the nearest one is in Puchong, where I had made a complaint about their service! So the only way I could transfer money to my Citibank savings account was through bank-to-bank transfer, and that costs RM2 per transaction (free in Australia).

It was a pity that I could not find a single Citibank ATM at the Changi International Airport, although there was a humongous annoying big Citibank bunting right in the middle of their departures terminal.

How deceiving that was! I ended up exchanging my Australian dollars (since Australian and Singapore currently have almost similar exchange rate) at the exchange bureau in the airport and at Chinatown (better cash rates), and not using my Citibank Visa Debit card thereafter.

Oh Well.

Australia: Myer One cardholders - More places to earn credit.

I've held a Myer card since my Toowoomba undergraduate days. Yet, I rarely used the card- as I barely did much shopping there. Granted, Myers is to the Aussies, what Isetan is to Malaysians. An upmarket retail establishment.

If I am not wrong, Coles & Myers used to be under one management.. and I used to take out my Coles card to collect the points. It was very much later that I realised that the point conversion was very much higher than what I was used to in Malaysia. It would take such a long time to collect points, that I decided to forgo bringing out the card altogether.

Currently, for a limited time period, Citibank Malaysia has launched a programme offering in exchange to its credit card-members the equivalency of 180 Citibank Reward Points to RM1.00 to be redeemed instantly at specific places.

Getting points as you buy- is a very asian thing, and currently practiced a lot by the Malaysian financial institutions for their credit card-members. It IS very evident in Japan, and South Korea, I realised when I was there. Malaysia and Singapore have yet to even compete on that level!

With this, I guess Australian shopping establishments are catching up on that practice now....

If you are a Myer One card holder, click here to find more places to collect those points!

Sunday, October 18, 2009

ING DIRECT Australia: Introducing Orange Everyday.

Originally just offering online banking products and services, ING Direct Australia is fast expanding and growing their services amidst the Global Financial Crisis. It definitely puts other established financial institutions to shame, and a run for their money!

If anyone should know, Australia is notorious for having banks that charge high monthly Transaction and Account-keeping fees that range from AUD6.00. Multiply that by 12 months, thats 12 months x AUD6 = AUD72.00! Killer Fees indeed!

Up to date, it is difficult at most Australian financial establishments to get an exemption of these fees unless the individual concerned

- is a "full time student- including international students",

- have a "working relationship" with the bank- whereby they have a deposit of a minimum amount- normally exceeding AUD50,000.00

- or, the bank just does not charge account-keeping fees!

ING Direct describes their newest financial product, Orange Everyday, as a "full fledged transaction account with all the features you expect.."

Its facilities include:

- No monthly account keeping fees.

- A Visa Debit card.

- EFTPOS facilities is available.

- Free unlimited online transactions- BPAY & Pay Anyone facilities

- Online bank cheques.

- Free use of every ATM in Australia when you withdraw AUD200 or more.

- Cash-Out Bonus (AUD0.50 cents) on EFTPOS of $200 or more.

It's definitely good news that ING Direct Australia is willing to provide fee-free during this time...

at least I do not have crack my head going around looking for more banks that offers such competitive facilities to SAVE on fees! ^^

For more information on this financial product, log on to their website.

Friday, October 16, 2009

Australia: Commonwealth Bank In Pink!

Commonwealth logo in PINK!!

Commonwealth logo in PINK!! I thought my eyes were playing with me when I saw the Commonwealth Bank logo in Pink...

Yes, we did have here, the towering and majestic Menara KL Tower recently lighting up in PINK for the entire month of October! But I thought that was only limited to Malaysia!

It's good to know that as usual, Australian institutions are showing the same care for womenfolk all over in conjunction with the Breast Cancer Awareness.

G'day on ya, Commonwealth Bank!!

Wednesday, October 14, 2009

Malaysia: Introducing Citibank Visa Debit

We have all heard of Citibank Visa & Mastercard Credit Cards.. *NOW*, Citibank Malaysia has finally released the Statement Brochure for their Visa Debit cards.

What used to be just a normal ATM card, now possess the priviledges of all the Visa benefits.

Citibank Malaysia is giving to all its Visa Debit card users:

- 8 X Citi Reward Points for Petrol Purchases nationwide

- 5 X Citi Reward Points for Grocery Purchases nationwide

- 3 X Citi Reward Points for Utility Bill Payments & Book Purchases nationwide.

Offer is valid from 1st Oct- 31st Dec 2009 unless stated.

*BENEFITS* from the Citibank Visa Debit

- 1 Citi Rewards Points for RM1 spent on the card for all other purchases.

- Ability to perform internet, mail and telephone order transactions.

- Free Citibank withdrawals at over 13,500 Citibank ATMs worldwide.

- Evergreen Citi Rewards Points.

- FREE Sign & Fly Protection.

- and more to come!!

Thursday, September 17, 2009

Tiger Airways: Flying to Singapore Cheap-Cheap.

After going through the hassle of checking out the different modes of transportation, I finally bought my tickets to Singapore. Tiger Airways is truly cheap, when every other normal cheap airlines could not!

It was even cheaper as I possessed a CommSec Australian issued debit MasterCard. For some reason or another, my RM12 credit/debit card fees were waived because of that! Wow.

RM139 - on a 10 hour one way- Kereta Api Tanah Melayu ride from Kuala Lumpur to Singapore.

RM90- for a four- five hour one way- bus coach ride from Kuala Lumpur to Singapore.

RM137- for a return journey on Tiger Airways Kuala Lumpur to Singapore.

It beat Air Asia by about RM200. My flights to Singapore return for this busy Raya festive time cost me RM137 (with no luggage) , and only free carry on 7 kgs luggage, taxes and everything included.

You might want to consider it after all. ^^

It was even cheaper as I possessed a CommSec Australian issued debit MasterCard. For some reason or another, my RM12 credit/debit card fees were waived because of that! Wow.

RM139 - on a 10 hour one way- Kereta Api Tanah Melayu ride from Kuala Lumpur to Singapore.

RM90- for a four- five hour one way- bus coach ride from Kuala Lumpur to Singapore.

RM137- for a return journey on Tiger Airways Kuala Lumpur to Singapore.

It beat Air Asia by about RM200. My flights to Singapore return for this busy Raya festive time cost me RM137 (with no luggage) , and only free carry on 7 kgs luggage, taxes and everything included.

You might want to consider it after all. ^^

Tuesday, September 15, 2009

And I"m Off To Singapore, Guys!

Hi readers, this is to inform you guys that I'd be away this coming weekend (19th-21st September) to Singapore for 3 Days 2 Nights. Well, that is, should everything go as intended.

With Raya around the corner, it was truly a last minute decision. I was not even sure if we'd be able to even get accomodation, nor transport to head down. But it seems that some ad-hoc trips could be sheer fun for the stress it produces! Heh. What with the Grand Prix F1 that will be on next week, and everything, I thought accomodation would be like looking for a needle in a haystack..

I'll be checking in at a budget accomodation, very near to a MRT (lucky us!), costing a mere SGD58 for a twin-bed sized room.

Along the way, I'll be there to check out their local spending habits, prominent banks and best credit cards.. and try not to break the bank on the credit card (as I've already overspent for this month already!!)

Okay, Ta-Ta! Enjoy your Raya holidays!

With Raya around the corner, it was truly a last minute decision. I was not even sure if we'd be able to even get accomodation, nor transport to head down. But it seems that some ad-hoc trips could be sheer fun for the stress it produces! Heh. What with the Grand Prix F1 that will be on next week, and everything, I thought accomodation would be like looking for a needle in a haystack..

I'll be checking in at a budget accomodation, very near to a MRT (lucky us!), costing a mere SGD58 for a twin-bed sized room.

Along the way, I'll be there to check out their local spending habits, prominent banks and best credit cards.. and try not to break the bank on the credit card (as I've already overspent for this month already!!)

Okay, Ta-Ta! Enjoy your Raya holidays!

Tuesday, September 1, 2009

Maybank Sony Credit Card: The Experience

So, how does it feel to possess a Maybank credit card in the past few weeks?

I realised that Maybank gives out Treat Points mostly for credit card usage, and not so much for the Visa Debit Card, which is 1 point for every RM3 spent. As it is so, somehow I have succumbed to what every typical person in malaysia who owns a credit card does. My Visa Debit has since been placed onto the shelf to rust.

Personally, I feel it is safer to use a credit card than a debit card, as consumers can always apply for a CHARGEBACK, but difficult in the case of a debit, or ATM card. Chargeback is the case where consumers may feel that they may not have liked a particular product, or service which they have bought, and decide to forgo it, and hence applies to the bank to reject the purchase/transaction that was made.

Because a Credit Card is basically using the bank's money, and is a loan from the bank's funds, at most times, they are more than willing to reverse the transaction. However, if it is the customer's own money from his savings, or current account, at most times, the bank may still perform the chargeback, however taking a longer period to do so, as it is not really their money.

As my credit card is linked to my account (which I can quickly scan through the amount that I owe the bank), it is easy for me to assign the portion of the amount due so that I would not overspend.

In order to not overspend, I have created psychological barriers that will intentionally present my account as one that is under-funded i.e. transferring it into a Term Deposit account away from harm's reach!

Pyschologically, it serves to deter me from over-spending when I go out.

I hope it works in the long run.

WHAT DO YOU THINK? DO YOU AGREE WITH ME?

I realised that Maybank gives out Treat Points mostly for credit card usage, and not so much for the Visa Debit Card, which is 1 point for every RM3 spent. As it is so, somehow I have succumbed to what every typical person in malaysia who owns a credit card does. My Visa Debit has since been placed onto the shelf to rust.

Personally, I feel it is safer to use a credit card than a debit card, as consumers can always apply for a CHARGEBACK, but difficult in the case of a debit, or ATM card. Chargeback is the case where consumers may feel that they may not have liked a particular product, or service which they have bought, and decide to forgo it, and hence applies to the bank to reject the purchase/transaction that was made.

Because a Credit Card is basically using the bank's money, and is a loan from the bank's funds, at most times, they are more than willing to reverse the transaction. However, if it is the customer's own money from his savings, or current account, at most times, the bank may still perform the chargeback, however taking a longer period to do so, as it is not really their money.

As my credit card is linked to my account (which I can quickly scan through the amount that I owe the bank), it is easy for me to assign the portion of the amount due so that I would not overspend.

In order to not overspend, I have created psychological barriers that will intentionally present my account as one that is under-funded i.e. transferring it into a Term Deposit account away from harm's reach!

Pyschologically, it serves to deter me from over-spending when I go out.

I hope it works in the long run.

WHAT DO YOU THINK? DO YOU AGREE WITH ME?

Saturday, August 15, 2009

Maybank: Paywave Terminal doesn't work.

Have you ever seen one of those yellow Maybank "paywave" terminals? They abound aplenty at most

Carrefour hypermarkets, and many other supermarkets out there.

Today I was at Carrefour Tropicana Mall to do some toiletries shopping. Upon arrival at the check-out counter, I decided to be cheeky, and decided to try using my Maybank SonyCard Visa card at the "Paywave" terminal.

Taking out the card, I decided to "wave" it....

once....

twice...

three times..

The check-out personnel said it sometimes works, it sometimes doesn't work.

How disappointing.

Installing ineffective, pretty useless "paywave" terminals that doesn't work half the time. So I had to pay the card by the normal way. Swipe the SIM into the terminal and SIGN.

*SIGH* What a waste of good money down the drain for prefectly useless "wave" contraptions, Maybank...

Carrefour hypermarkets, and many other supermarkets out there.

Today I was at Carrefour Tropicana Mall to do some toiletries shopping. Upon arrival at the check-out counter, I decided to be cheeky, and decided to try using my Maybank SonyCard Visa card at the "Paywave" terminal.

Taking out the card, I decided to "wave" it....

once....

twice...

three times..

The check-out personnel said it sometimes works, it sometimes doesn't work.

How disappointing.

Installing ineffective, pretty useless "paywave" terminals that doesn't work half the time. So I had to pay the card by the normal way. Swipe the SIM into the terminal and SIGN.

*SIGH* What a waste of good money down the drain for prefectly useless "wave" contraptions, Maybank...

Tuesday, August 4, 2009

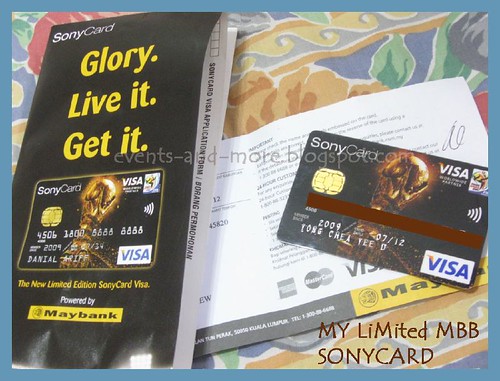

Maybank: My "Limited SonyCard"

After a week being away from Kuala Lumpur, I finally managed to go to the bank to pick up my newly approved Limited Maybank SonyCard!

Look at how cool it looks?

Anyways, it's only for emergencies. With Finance Charges of up to 1.46%, and Late Payment Charges of 1%, I think it's better to only use it for those times when its necessary, i.e. big amount purchases to be covered by insurance, or when I have limited funds in my savings account. LOL.

Friday, July 31, 2009

Maybank: Limited Version "SonyCard" Application Approved!

Recently, during the Maybank Treats Fair at Mid Valley, I decided to put in an application for credit card. There were a number of credit cards on showcase, so it took me a while to decide which card to apply for.

Finally, the consultant then informed that I could put in an application for a few cards, and the credit card processing department will choose one that I was most qualified for. So, I decided to put in an application for not only the Limited Version "SonyCard", but the American Express Gold Credit Card as well.

After waiting for two days, I received a text message on my mobile informing me that my application for the card was approved!

The card comes with exclusive Sony discounts, extended warranty, sale previews and more. Among its features include:

* Free For Life No Annual Fee.

* Up to 24 months' extended warranty on Sony products

* Built-in Visa Wave feature: just wave and go!

*10X Treat Points when purchasing Sony products at Sony Style, Sony Centre and selected Sony Designated Stores

Anyways, as I had only just started working in Malaysia recently, I was told only to provide

Since I was away when I received the text message, and had only just returned from Penang, I called the bank, and was informed that they still had the card with them, and would be forwarding the card to my home-branch for collection.

Oh well. Better safe than sorry sometimes. ^^ Can't wait to get my card!

Finally, the consultant then informed that I could put in an application for a few cards, and the credit card processing department will choose one that I was most qualified for. So, I decided to put in an application for not only the Limited Version "SonyCard", but the American Express Gold Credit Card as well.

After waiting for two days, I received a text message on my mobile informing me that my application for the card was approved!

The card comes with exclusive Sony discounts, extended warranty, sale previews and more. Among its features include:

* Free For Life No Annual Fee.

* Up to 24 months' extended warranty on Sony products

* Built-in Visa Wave feature: just wave and go!

*10X Treat Points when purchasing Sony products at Sony Style, Sony Centre and selected Sony Designated Stores

Anyways, as I had only just started working in Malaysia recently, I was told only to provide

- A copy of 3 months pay-slip (original).

- A copy of my job offer from my Employer (original)

- A photocopy of my university degree (which was certified, in my case).

Since I was away when I received the text message, and had only just returned from Penang, I called the bank, and was informed that they still had the card with them, and would be forwarding the card to my home-branch for collection.

Oh well. Better safe than sorry sometimes. ^^ Can't wait to get my card!

Maybank Visa Debit: Online Shopping Enabled!

When Maybank Visa Debit was introduced to the Malaysian public, the people who used Paypal thought they'd finally have found another card for online shopping...

However, that took about another 12 months before that wish became a viable option..

Finally in the first week of July 2009, Maybank announced that Visa Debit was going online, a week after announcing the online enhancement security for their Credit Cards.

3 Easy Steps to register your Maybankard Visa Debit for online purchase:

However, that took about another 12 months before that wish became a viable option..

Finally in the first week of July 2009, Maybank announced that Visa Debit was going online, a week after announcing the online enhancement security for their Credit Cards.

3 Easy Steps to register your Maybankard Visa Debit for online purchase:

Step 1 :

Login to Maybank2u.com and select Maybankard Secure Online Shopping Registration. Select "Utilities" function.Step 2 :

Complete the enrolment process by entering the following information :

- Card Number

- MSOS Password

- Confirm MSOS Password

- PAM (Personal Assurance Message)

- Expiry Date

- CVV Number

- Hint Question

- Hint Answer

- View screenshot

Step 3 :

Successful registration notification message will appear once registration is successful and complete.

Click here for more details.

Saturday, July 25, 2009

Malaysia: Credit Cards Application (Part 1)

At the Maybank Treats Fair recently, their bank recently decided to up the Annum Income for ALL their Maybank cards to RM30,000.00 per year. They were also promoting their American Express Gold Credit Card and Limited Edition Sony Card. Both are Annual Fee-Free!

So I decided to have a look at the banks with their available cards for the new applicant. The information is gathered from the respective banks' websites.

All information is technically "correct" as of date of this entry. Please refer to the respective banks for more information before putting in a credit card application.

HSBC

Classic Cards- Mastercard or Visa

Income Per Annum: RM18,000.00

Annual Fee: RM80

Joining Fee: Waived.

CITIBANK

Choice Credit Card

Income Per Annum: RM18,000.00

Annual Fee: Nil - Subject to 2x transactions a month, otherwise a RM5.00 monthly fee will be charged.

Clear Card

Income Per Annum: RM18,000.00

Annual Fee: RM90.00

Gold Credit Card

Income Per Annum: RM 36,000

Annual Fee: RM195.00

Cash Back Credit Card

Income Per Annum: RM18,000.00

Annual Fee: RM90.00

EON BANK:

Classic Cards:

Income Per Annum: RM18,000.00

Gold Card:

Income Per Annum: RM30,000.00

Visa Wave' n Go Credit Card:

Classic

Income Per Annum: RM18,000

Gold

Income Per Annum: RM32,000

PUBLIC BANK

Classic Visa/Mastercard

Income Per Annum: RM18,000

Annual Fee: RM75

Gold

Income Per Annum: 25,000.00

Annual Fee: RM150

HONG LEONG

Classic Card

Income Per Annum: RM18,000.00

Annual Fee:

American Express:

Income Per Annum: RM18,000.00

Annual Fee:

American Express Gold

Income Per Annum: RM36,000.00

Annual Fee:

CIMB

(to be continued.....)

So I decided to have a look at the banks with their available cards for the new applicant. The information is gathered from the respective banks' websites.

All information is technically "correct" as of date of this entry. Please refer to the respective banks for more information before putting in a credit card application.

HSBC

Classic Cards- Mastercard or Visa

Income Per Annum: RM18,000.00

Annual Fee: RM80

Joining Fee: Waived.

CITIBANK

Choice Credit Card

Income Per Annum: RM18,000.00

Annual Fee: Nil - Subject to 2x transactions a month, otherwise a RM5.00 monthly fee will be charged.

Clear Card

Income Per Annum: RM18,000.00

Annual Fee: RM90.00

Gold Credit Card

Income Per Annum: RM 36,000

Annual Fee: RM195.00

Cash Back Credit Card

Income Per Annum: RM18,000.00

Annual Fee: RM90.00

EON BANK:

| For Salary Earner: | |

| Latest Salary Slip OR | |

| Latest EA Form OR BE Form (together with payment receipt if any, to Lembaga Hasil Dalam Negeri) | |

For Commission Earner: | |

| Latest 3 months Commission Slip OR Salary Slip | |

| Latest BE Form (together with payment receipt if any, to Lembaga Hasil Dalam Negeri) | |

| | |

Income Per Annum: RM18,000.00

Gold Card:

Income Per Annum: RM30,000.00

Visa Wave' n Go Credit Card:

Classic

Income Per Annum: RM18,000

Gold

Income Per Annum: RM32,000

PUBLIC BANK

Classic Visa/Mastercard

Income Per Annum: RM18,000

Annual Fee: RM75

Gold

Income Per Annum: 25,000.00

Annual Fee: RM150

HONG LEONG

Classic Card

Income Per Annum: RM18,000.00

Annual Fee:

American Express:

Income Per Annum: RM18,000.00

Annual Fee:

American Express Gold

Income Per Annum: RM36,000.00

Annual Fee:

CIMB

(to be continued.....)

Monday, July 20, 2009

A Receipt is Important for Purchases.

Today, I found a great link for customers who want to return objects/gifts/purchases without a receipt, especially those times when it was a gift, or we lost the receipt.

How To Return Anything (Without A Receipt)

How To Return Anything (Without A Receipt)

Tuesday, July 14, 2009

Citibank: Visa Debit charges for foreign transactions.

On Sunday (12th July), I sent an enquiry to Citibank online Customer Service, and received a reply yesterday (13th July).

My queries were:

My queries were:

I would like to ask what would be the charges payable for using the Citibank ATM card for transactions made overseas?And the reverted reply was:

Transactions as in:

1) Purchases made in a retail shop, what are the charges payable?

2) Withdrawals overseas from non-Citibank ATM?

3) Withdrawals overseas

That's a VERY good reason to start using Citibank ATM Debit Visa overseas if I won't be charged conversion fees per transaction, or any fees per transaction!

There are no Debit & ATM card specific charges. There is no charges if the withdrawal is made from an overseas Citibank ATM machine. However, RM10.00 will be charged per withdrawal if made via other network (PLUS, NYCE,STAR ). However, we are not able to advise the equivalent amount in RM for withdrawal in foreign currency as the rates used are not Citibank's quoted rates.

Please kindly note that the usage of Citicard for Islamic Banking and Flexihome Loan customers is restricted to Citbank Malaysia only.

Citibank: Experience at the Puchong Branch.

I finally received my first ever statement for my Malaysian Citibank Savings Acct. statement! I had read somewhere on the Internet that it was difficult to even apply for a savings account in Citibank. Yes, and almost all of that story is true, at least from my experience.

SERVICE NOT UP TO EXPECTATION.

The person who had served me was a Chinese male in the Puchong branch, in his mid 20s to early 30s. I had gone to Puchong to service a client's company, and as there was a branch there, I decided to head over to open an account of the convenience of the location.

But I was not expecting the kind of service that was to be rendered by the staff, who I shall address as "L". I deposited RM250.00 into my account. It was only after depositing the money, and getting my so-called "bank-in slip", and leaving the outlet that I realised that he didn't even provide me the details of my savings account number.

As for the ATM card, I was not even given any information about when it would arrive or how I would get it. So after a week, I called up the Citibank Helpline to enquire about the ATM card, as I thought it would be normal procedure for banks to send cards to the customer's mailing address. I was then informed by the Helpline phone personnel that I could have the card created "on-the-spot" at any Citibank outlet, or sent by mail.

The person who managed my call, was even more surprised to know that I wasn't given the account number, and ATM card. Then she informed me that there was no directive in the Citibank system to create the ATM card!

It was an atrocious service coming from a service-related industry provider, and especially from an International bank like Citibank. Never had I experienced such atrocious service even when opening a new saving accounts at my local Maybank branch.

FOLLOW-UP TO GRIEVANCE PROCESS

Furious, I then forwarded a lengthy e-mail to the Customer Service Dept., of which response time took about 5 days. The Customer Representative waived the Courier fees for my ATM card, but the Processing Fee could not be waived, which was RM8.

I was quite happy, mostly because I did not have to take time off just to return to the Puchong branch to have my card created. To do that, I'd have to get someone to drive me (or borrow someone's car) and take time off during lunch hours for that very purpose.

A few days later, I received in the mail, a Customer Service feedback form which I promptly filled in and sent it off again.

REFLECTION

I'm just happy to not have to waste my time to go all the way to the bank. I had written the letter out of disatissfaction, but happy out of the knowledge that I was not just one who complained but did not do anything about it.

Yes, and also the knowledge that another staff at the Customer Service of an international bank learns the importance of good relationship manners. Which I hope he does know by now what that entails if he performs poorly!

Taxes for Adsense Payments: Malaysia or Australia?

I just realised that I will have to pay taxes for adsense payments.

The only question is, "what is the amount?", as a search through the Internet has not provided much information on how to pay taxes on this.

As for declaring it as income, it is a question of whether to declare it to the Australian ATO, or Malaysian Income Taxes, depending on whether payment is to be made through EFT to Australian banks, or by cheque in Malaysia.

Of course, in Australia, the level of taxes to be paid is much higher. As for how much taxes, that really depends how much I can get... Hahaha..

It might take another six months before I can even get a payment for Adsense payment (if I ever get it anyways!), so by that time, Google might have come up with an alternate payment method then.

^^

The only question is, "what is the amount?", as a search through the Internet has not provided much information on how to pay taxes on this.

As for declaring it as income, it is a question of whether to declare it to the Australian ATO, or Malaysian Income Taxes, depending on whether payment is to be made through EFT to Australian banks, or by cheque in Malaysia.

Of course, in Australia, the level of taxes to be paid is much higher. As for how much taxes, that really depends how much I can get... Hahaha..

It might take another six months before I can even get a payment for Adsense payment (if I ever get it anyways!), so by that time, Google might have come up with an alternate payment method then.

^^

Sunday, July 12, 2009

"Bring Your Own Bento" to Office: Mission Accomplished!

I have now officially passed my 10th day (In translation = 2 weeks) of bringing a bento to office for my mid-day meal.

After about the first five days of bringing a plastic base square food containers, I switched to using the normal typical Malaysian tiffin food carrier.

Why?

1) Convenience- Plastic base food containers require the use of hot water to remove the oil surface from contact with prepared food that has oil properties, whereas oil does not stick to the surface of the metal tiffin carrier. It really is a time waster.

2) Healthier- I don't have to be worried about eating the oil that may stick to the surface of a tiffin carrier, as that would not happen.

One of the male staff had not washed his plastic bowl after his meals with hot water, and just merely washed it with dish detergent. There were ants crawling all over it!

So yes, Mission Accomplished! I have managed to save some money by bringing my own lunch. However, apart from that too, my main purpose was to eat healthily, and I really need to remind myself that I have to consume less rice so as to lose those kilos which is hazardous being carbs for the physical state of my body that is!!!

If you're wondering, a lot of Australians do bring their own lunch to work. Eating out is very expensive, and a meal out (even at the fairly cheap Hungry Jack's/Burger King) could set you down by AUD6- 8. Hence, it's not uncommon to see many people bring lunchboxes to workplaces. Occassionally, they may eat out, but it's not so common to have lunch out like what you may see in Malaysia.

Many of my friends in Australia bring their own lunch to work. We normally cook for about three day's meal in a row, put them in lunch boxes, and then re-heat them for the day that we need to eat it. Saves heaps of money in that manner. It's just a bit less common to see that happening in Malaysia though... since food here is heaps much more cheaper anytime.

Though so, dinner maybe a different story...

After about the first five days of bringing a plastic base square food containers, I switched to using the normal typical Malaysian tiffin food carrier.

Why?

1) Convenience- Plastic base food containers require the use of hot water to remove the oil surface from contact with prepared food that has oil properties, whereas oil does not stick to the surface of the metal tiffin carrier. It really is a time waster.

2) Healthier- I don't have to be worried about eating the oil that may stick to the surface of a tiffin carrier, as that would not happen.

One of the male staff had not washed his plastic bowl after his meals with hot water, and just merely washed it with dish detergent. There were ants crawling all over it!

So yes, Mission Accomplished! I have managed to save some money by bringing my own lunch. However, apart from that too, my main purpose was to eat healthily, and I really need to remind myself that I have to consume less rice so as to lose those kilos which is hazardous being carbs for the physical state of my body that is!!!

If you're wondering, a lot of Australians do bring their own lunch to work. Eating out is very expensive, and a meal out (even at the fairly cheap Hungry Jack's/Burger King) could set you down by AUD6- 8. Hence, it's not uncommon to see many people bring lunchboxes to workplaces. Occassionally, they may eat out, but it's not so common to have lunch out like what you may see in Malaysia.

Many of my friends in Australia bring their own lunch to work. We normally cook for about three day's meal in a row, put them in lunch boxes, and then re-heat them for the day that we need to eat it. Saves heaps of money in that manner. It's just a bit less common to see that happening in Malaysia though... since food here is heaps much more cheaper anytime.

Though so, dinner maybe a different story...

Adsense Earnings: Now In Australian Dollars!

Did you know that you can now be paid in Australian Dollars for Adsense Payments?

Well, at least that is the case for me. I was in Australia for the last three years, so in total, I have a Savings Account with

1) Commonwealth Bank (maintenance is AUD6 per month).

2) Commonwealth Securities (where maintainence is Fee-Free & comes with a fee-free ATM & Debit MasterCard)

3) HSBC Bank.(fee free and comes with a fee-free ATM & Debit Visa Card)

4) Heritage Building Society (has the functions almost similar to a bank, and is fee-free as well).

That's FOUR banks in total!

For payment in Australian Currency, the Adsense Payment will be banked in straight away into your account electronically, and it has to be a minimum of AUD150 before payment can be made.

So, I changed all my payment to be transferred to Commonwealth Bank, being that Google has a working relationship with Australian banks to transfer payment immediately. Nonetheless, its still my account, so I am fine with payment with transferred into the account there, since I have the means of an ATM card to withdraw the total AUD150 in Malaysia if I ever needed to. ^^

Well, at least that is the case for me. I was in Australia for the last three years, so in total, I have a Savings Account with

1) Commonwealth Bank (maintenance is AUD6 per month).

2) Commonwealth Securities (where maintainence is Fee-Free & comes with a fee-free ATM & Debit MasterCard)

3) HSBC Bank.(fee free and comes with a fee-free ATM & Debit Visa Card)

4) Heritage Building Society (has the functions almost similar to a bank, and is fee-free as well).

That's FOUR banks in total!

For payment in Australian Currency, the Adsense Payment will be banked in straight away into your account electronically, and it has to be a minimum of AUD150 before payment can be made.

So, I changed all my payment to be transferred to Commonwealth Bank, being that Google has a working relationship with Australian banks to transfer payment immediately. Nonetheless, its still my account, so I am fine with payment with transferred into the account there, since I have the means of an ATM card to withdraw the total AUD150 in Malaysia if I ever needed to. ^^

Monday, June 29, 2009

Bento Lunch Challenge: Day 1

I finally got up at 7.30am this morning..

Took 15 mins to warm up the azuki-bean stew we made last night. Another 2 mins to warm up the food in the lunchbox. Then realised I needed to find something to keep the lunch box insulated...

Had to search for a "furoshiki" - bento wrap, as the microwave in the next door office was out of service.. Finally found a cooler bag.. well, anything, as long as it works!

Next had to add sugar to the simmering azuki bean-stew on the pot. It was bland without any taste! Then, drank my Earl Grey tea, and left my morning azuki bean stew to cool down.

It's already almost 9am. Need to get ready to go to office now.

Took 15 mins to warm up the azuki-bean stew we made last night. Another 2 mins to warm up the food in the lunchbox. Then realised I needed to find something to keep the lunch box insulated...

Had to search for a "furoshiki" - bento wrap, as the microwave in the next door office was out of service.. Finally found a cooler bag.. well, anything, as long as it works!

Next had to add sugar to the simmering azuki bean-stew on the pot. It was bland without any taste! Then, drank my Earl Grey tea, and left my morning azuki bean stew to cool down.

It's already almost 9am. Need to get ready to go to office now.

The RM10 Per Day Challenge.

Recently, I have been using too much of my ATM card for frivolous impulse purchases.

As I couldn't trust myself (to not be a Shopoholic), I have resorted to keeping a huge watch on my purchases.

Hence, I have decided to bring "bento lunch" to office for the next 14 days, and see how I cope. As I won't be spending any money on lunch, then in my wallet there shall be a maximum of RM10 at all times. (I average about RM5.50 for economy rice for lunch (with meat). Without meat, it would be about RM3.70).

My "bento lunch" will consist of rice, egg, and some vege. Healthy. But necessary to manage the pounds that I am putting on!

So, RM10 should be adequate for my daily expenses unless there was an emergency purchase, or I had a prior appointment that I had made. In that case I will then "recharge" my wallet to the necessary amount to ensure that I have enough to use for the outing.

Wish Me Luck!

As I couldn't trust myself (to not be a Shopoholic), I have resorted to keeping a huge watch on my purchases.

Hence, I have decided to bring "bento lunch" to office for the next 14 days, and see how I cope. As I won't be spending any money on lunch, then in my wallet there shall be a maximum of RM10 at all times. (I average about RM5.50 for economy rice for lunch (with meat). Without meat, it would be about RM3.70).

My "bento lunch" will consist of rice, egg, and some vege. Healthy. But necessary to manage the pounds that I am putting on!

So, RM10 should be adequate for my daily expenses unless there was an emergency purchase, or I had a prior appointment that I had made. In that case I will then "recharge" my wallet to the necessary amount to ensure that I have enough to use for the outing.

Wish Me Luck!

Sunday, June 28, 2009

Consumer Protection: Cases of Unscrupulous Home Product Providers.

This blog entry is the continuation of this entry.

All Cases quoted here are taken from:

TTPM (May 2008), "Mudah Murah & Cepat- Claim Your Consumer Rights".